Introduction

US companies shipping medical products to India often get hit with an unexpected cost when those goods come back: US import duties charged a second time, even on items originally made in or exported from the United States. CBP treats all arriving merchandise as new imports subject to duty unless the importer actively claims an exemption.

According to CBP's official guidance on HTS 9801, there is no automatic recognition of returned goods — duty-free treatment must be affirmatively claimed at entry.

India's zero de minimis threshold compounds the problem: every outbound shipment faces full Indian import duties on arrival, so by the time goods return to the US, importers have already absorbed significant international duty costs. Without proper documentation and classification, companies end up paying duties twice on the same products.

What follows covers why double-duty situations occur, how to use HTS 9801 to re-import returned goods duty-free, and what documentation and conditions determine eligibility.

TL;DR

- HTS 9801.00.10 lets US-exported goods return duty-free, but you must actively claim it — CBP won't apply it automatically

- US-origin goods have no time limit; foreign-origin goods must return within 3 years, unaltered

- Goods must return in the same condition, with no repairs or modifications made while in India

- You'll need proof of original US export, an Importer's Declaration, and a Foreign Shipper's Declaration

- Shipments over $2,500 require formal entry through a licensed customs broker

Why Goods Returned from India Get Hit with Double US Customs Duties

When a US company exports goods to India, those goods leave without paying US export duties. However, when they return, CBP treats them as arriving imports and assesses duties unless the importer actively claims an exemption under HTS 9801.

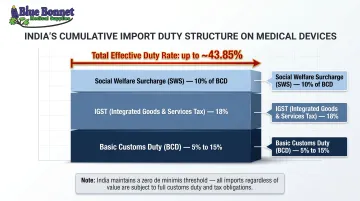

India's customs environment adds costs before goods even start the return journey. India maintains a zero INR de minimis threshold, meaning every commercial shipment arriving in India faces full duty assessment. According to the WTO India Tariff Profile 2024, India's simple average MFN applied tariff is 16.2% overall. For medical devices, the charges stack up quickly:

- Basic Customs Duty (BCD): 5%–15% depending on device classification

- IGST: typically 18%

- Social Welfare Surcharge: 10% applied on top of BCD

HTS 9801 is a classification under the US Harmonized Tariff Schedule that provides duty-free re-entry for goods previously exported from the US and returning in the same condition. This provision is distinct from duty drawback — drawback recovers duties on exports after the fact, while 9801 prevents new duties from being assessed on returning goods at the point of entry.

The Trade Facilitation and Trade Enforcement Act of 2015 expanded HTS 9801.00.10 to cover both US-origin products returned after export (no time limit) and foreign-origin products returned within 3 years. The exemption is never applied automatically, though. The importer must claim it with proper documentation at the time of entry.

How to Re-Import Returned Goods from India Without Paying Duplicate Duties

Successfully avoiding double duties requires deliberate action at each stage—before export, during the return shipment, and at US customs entry. Each step builds on the last; missing one can result in CBP assessing full duties on goods that would otherwise qualify for duty-free treatment.

Step 1: Confirm Eligibility Before the Return Ships

Before goods leave India, verify:

- Original US export documentation exists showing the goods were exported from the United States (not just manufactured there)

- Origin and time limits are met: US-origin goods have no time limit; foreign-origin goods must return within 3 years of the original export date

- No alterations occurred in India: Goods have not been repaired, modified, or improved in value while abroad, as any such change disqualifies them from HTS 9801 treatment

- Serial numbers or lot numbers match original export records to connect returning goods to the specific export event

For medical device companies, this verification is critical. Any work performed in India that CBP considers an "advancement in value" eliminates duty-free eligibility, and FDA may also treat it as remanufacturing—triggering full manufacturer obligations.

Step 2: Secure Export Proof Before Goods Leave India

The exporter in India (or your logistics partner) must provide:

- Commercial invoice or packing list from the original US export

- Airway bill or bill of lading number from when goods left the US

- Foreign Shipper's Declaration: A signed statement from the party returning the goods affirming that:

- The items are the same goods previously exported from the US

- They have not been altered or advanced in value abroad

- The port and approximate date of original US export

According to 19 CFR 10.1, this declaration must be in English or accompanied by a certified translation.

Step 3: Prepare the Importer's Declaration

The US importer of record must prepare an Importer's Declaration stating:

- The goods being returned are the same goods previously exported from the United States

- They are in the same condition and have not been advanced in value or improved while abroad

- The name and location of the US manufacturer (if applicable)

- The articles were exported without benefit of drawback

This is a required document under 19 CFR 10.1(a)(2) for claiming HTS 9801 and must accompany the customs entry.

Step 4: File a Formal Customs Entry Under HTS 9801

Shipments valued over $2,500 require a formal entry filed through a licensed US customs broker. The broker must:

- Classify the goods under HTS 9801.00.10 (which covers both US-origin goods and foreign-origin goods returned within 3 years under the TFTEA 2015 expansion)

- File CBP Form 3461 (Entry/Immediate Delivery) at arrival

- File CBP Form 7501 (Entry Summary) within 10 working days of cargo release

- Obtain a customs bond (required for all formal entries over $2,500)

The 9801 claim must be made at the time of entry, not retroactively. Once an entry is liquidated without a 9801 claim, reversing it requires filing a formal protest within 180 days, which is time-consuming and CBP can deny it.

For medical products specifically, FDA admissibility requirements apply on top of CBP requirements. The goods must still meet FDA clearance standards upon re-entry, including registration/listing verification and premarket authorization.

Step 5: Respond to Any CBP Examination or Requests for Additional Documentation

CBP may physically examine the returned goods or request additional documentation to verify the "same condition" requirement. If CBP assesses duty that the importer believes is not owed, you can file a protest within 180 days after liquidation using CBP Form 19.

According to 19 USC 1514(c)(3), the protest window is strict: miss it, and you lose all ability to challenge the duty assessment.

What You Need Before Filing for Duty-Free Re-Entry

Assembling the right documentation before goods reach the US port of entry is the most controllable factor in avoiding double duties. CBP rarely reverses duty assessments once made — gaps in documentation are difficult to correct after the fact.

Export Records

Required documents include:

- Original commercial invoice from when goods were exported to India

- Airway bill or ocean bill of lading from that original export

- Automated Export System (AES) ITN if the export value exceeded $2,500

According to 15 CFR 30.2, Electronic Export Information (EEI) must be filed through AES for any export shipment where the value of the commodity under a single Schedule B number exceeds $2,500. The ITN serves as proof of export when claiming duty-free re-entry.

Companies using a compliant 3PL partner to manage outbound shipments will have these records readily accessible when a return occurs.

Return Shipment Documents

Required from the Indian side:

- Foreign Shipper's Declaration confirming the goods are unaltered

- Commercial invoice for the return shipment, referencing the original export

- Packing list matching the original shipment quantities and descriptions

The shipper's declaration must be in English or accompanied by a certified translation.

With documents in hand from both sides, the next step is formal entry filing — which carries its own requirements depending on shipment value.

Entry Filing Requirements

For shipments over $2,500:

- A licensed US customs broker must file the formal entry

- A customs bond (CBP Form 301) is required to secure payment obligations

- For medical products, FDA admissibility requirements apply in addition to CBP requirements

Companies working with a 3PL experienced in FDA-regulated goods — like Bluebonnet Medical Supplies — benefit from established broker relationships and compliance workflows already built into the return process.

Key Conditions That Determine If Your Return Qualifies Under HTS 9801

HTS 9801 eligibility is not simply a matter of paperwork—four substantive conditions must be met, and failure on any one eliminates duty-free treatment.

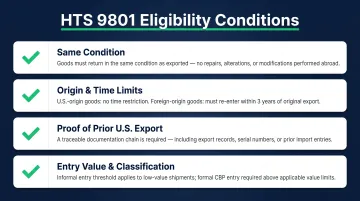

Condition 1: Same Condition

Goods must return in the exact same condition as when they left the US. For medical devices, this means:

- No repairs, reprocessing, sterilization changes, or modifications were performed in India

- Repair returns do not qualify under HTS 9801 and will be assessed duty as new imports

Note that "same condition" does not mean "unused"—a product can have been used in India and still qualify under 9801, as long as it was not altered. According to 19 CFR 10.1, goods must be returned "without having been advanced in value or improved in condition by any process of manufacture or other means while abroad."

The following activities generally do not disqualify goods:

- Cleaning and testing

- Inspecting and repacking

- Simple maintenance

Condition 2: Origin and Time Limits

- US-origin goods (manufactured in the US): No time limit for return

- Foreign-origin goods (most medical devices manufactured in Asia or Europe and first imported into the US): Must return within 3 years of the original US export date

This 3-year requirement is embedded in the HTS 9801.00.10 text under the TFTEA 2015 expansion.

Condition 3: Proof of Prior US Export

The goods must have been exported from the United States, not simply shipped through the US. The importer must connect the returning goods to a specific, documented export event using:

- Consistent product identifiers (serial numbers, lot numbers, SKU references)

- Documentation that appears on both original export documents and return shipment documents

- AES/ITN record linking the re-imported goods to the original export

Without this traceable connection, CBP has no basis to confirm the goods are the same items previously exported.

Condition 4: Entry Value and Classification

- Informal entry (below $2,500): Simpler process but still requires the 9801 claim to be made

- Formal entry (above $2,500): Requires a customs broker and a CBP bond

For medical product companies dealing with high-value device returns, formal entry is typically required. According to CBP bond requirements, the bond amount typically equals entered value plus duties/taxes, or three times value if subject to FDA or other agency requirements.

Common Mistakes That Lead to Double Duty Charges on India Returns

Three mistakes account for most double-duty situations on returned goods from India:

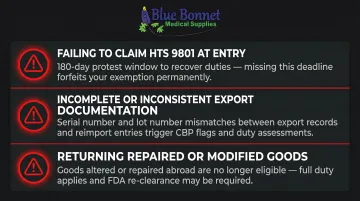

Failing to claim HTS 9801 at entry. CBP does not apply the exemption automatically — you must claim it. Once an entry is liquidated without a 9801 claim, reversing it requires a formal protest within 180 days under 19 USC 1514(c)(3), and approval is not guaranteed.

Incomplete or inconsistent export documentation. If serial numbers, product descriptions, or shipment records don't match across documents, CBP has no basis to confirm the returning goods are the same items that left the US. Documentation chains need to be established before goods leave — not assembled after the fact.

Returning goods that were repaired or modified abroad. Sending a medical device to India for repair, calibration, or a software update disqualifies it from 9801 treatment. According to FDA guidance on remanufacturing, any work that significantly changes a device's performance, safety specifications, or intended use may also trigger full FDA pre-market submission requirements before re-entry.

Frequently Asked Questions

Do I have to pay customs duty on items shipped from India to the United States?

Goods arriving from India are generally subject to US customs duties based on their HTS classification and country of origin. However, goods previously exported from the US may qualify for duty-free re-entry under HTS 9801 if they meet eligibility conditions: same condition, proper documentation, and applicable time limits.

Are U.S.-origin goods returning to the United States subject to customs duty?

US-origin goods returning from India are not subject to duty under HTS 9801.00.10, provided they return in the same condition and the importer can document the prior US export. No time limit applies to US-origin goods under this provision.

How do I declare duty-free purchases when returning to the United States?

For commercial return shipments, classify goods under HTS 9801.00.10 on the customs entry, supported by an Importer's Declaration and Foreign Shipper's Declaration. Shipments over $2,500 require a licensed customs broker — this process differs entirely from declaring personal purchases at the border.

What documentation do I need to re-import returned goods from India duty-free?

You'll need the following, with consistent product identifiers across all documents:

- Original export commercial invoice

- Airway bill or bill of lading from the US export

- Importer's Declaration

- Foreign Shipper's Declaration from the Indian exporter

- Return shipment commercial invoice and packing list

What is the time limit for claiming duty-free re-entry on goods returned from India?

US-origin goods have no time limit. Foreign-origin goods that were previously in the US must return within 3 years of the original US export date to qualify under HTS 9801.00.10. Goods returned after 3 years will be assessed duty as new imports.

What happens if returned medical goods from India were repaired or altered while abroad?

Goods repaired, modified, or improved in value while in India no longer meet the "same condition" requirement for HTS 9801 and will be assessed duty as new imports. For medical devices, alterations may also trigger FDA re-clearance obligations — confirm both customs and regulatory requirements before sending goods abroad for servicing.